Breaking the Debt Cycle: Better Alternatives to Payday Loans with Lower Interest and Flexible Terms

Imagine it is a rainy Tuesday afternoon, and you are staring at a car repair bill that costs more than your entire checking account balance. Your next paycheck is ten days away, and the panic begins to set in. For many, this is the moment they turn to a payday loan storefront. The promise of instant cash with ‘no credit check’ sounds like a lifeline. However, that lifeline often turns into a lead weight. Payday loans, known for their astronomical annual percentage rates (APRs) that can soar above 400%, are designed to be short-term fixes that lead to long-term debt traps.

But the narrative doesn’t have to end in a cycle of debt. There are numerous alternatives available today that offer the same speed and convenience as a payday loan but with significantly lower interest rates and terms that actually respect your financial well-being. This guide explores the most viable paths toward financial relief without the predatory baggage.

[IMAGE_PROMPT: A person sitting at a wooden desk with a laptop and a cup of coffee, looking relieved while looking at a mobile phone screen displaying a green financial growth chart, soft natural lighting.]

The Credit Union Advantage: Payday Alternative Loans (PALs)

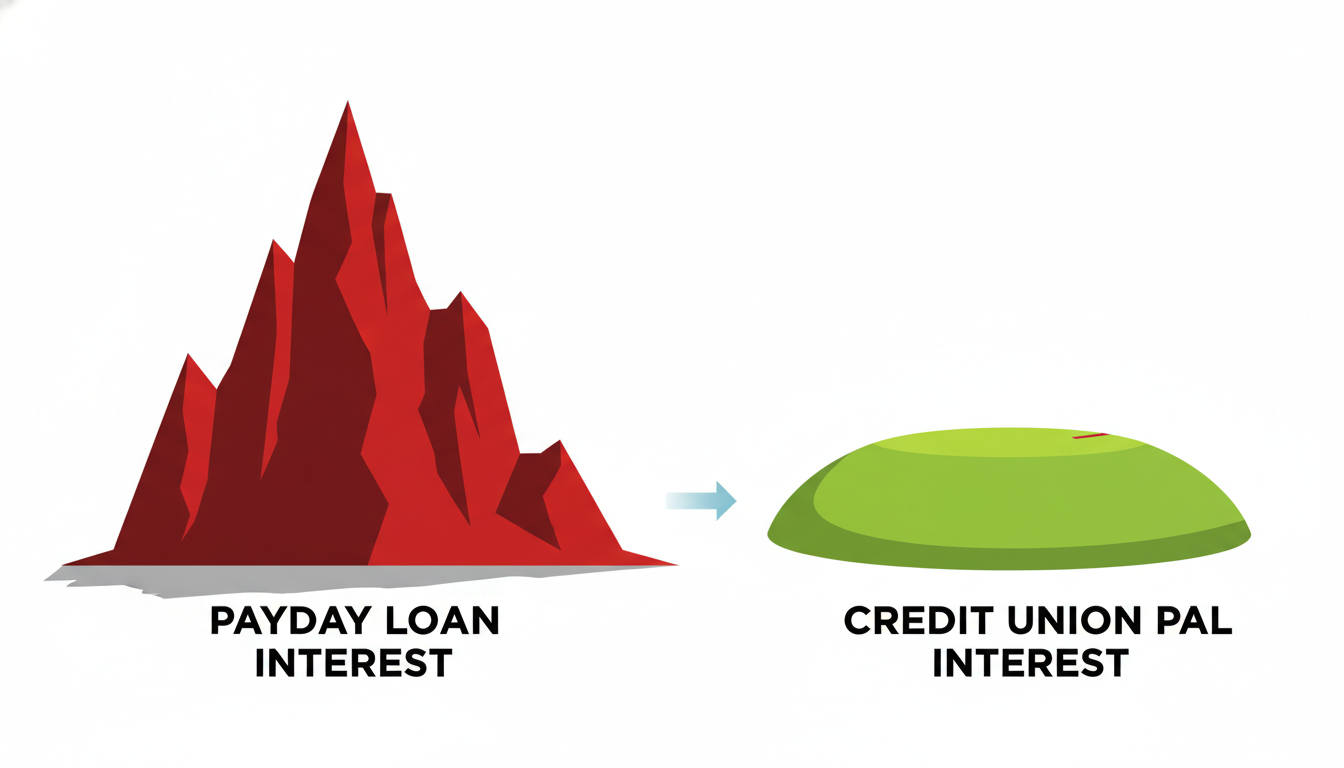

One of the most effective ways to bypass predatory lenders is through federal credit unions. Many offer what are specifically called Payday Alternative Loans (PALs). These loans were designed by the National Credit Union Administration (NCUA) as a direct response to the payday loan crisis. Unlike typical payday lenders who might charge $15 to $30 for every $100 borrowed, PALs cap their interest rates at 28%.

Furthermore, the terms are far more flexible. While a payday loan usually demands full repayment within two weeks, a PAL allows for repayment periods ranging from one to six months. This flexibility ensures that the monthly payment fits within a standard budget rather than swallowing an entire paycheck whole. To qualify, you generally need to be a member of the credit union for at least one month, making this a great option for those who plan ahead for potential emergencies.

The Rise of Fintech: Cash Advance and Earned Wage Apps

In the digital age, technology has paved the way for ‘Earned Wage Access’ (EWA). Apps like Earnin, Dave, and Brigit have revolutionized how workers access their money. Instead of borrowing against a future paycheck at a high cost, these apps allow you to withdraw money you have already earned but haven’t been paid yet.

Most of these apps operate on a ‘tip’ model or a small monthly subscription fee rather than traditional interest. For example, if you’ve worked 20 hours this week, you might be able to withdraw $100 of those earnings for a small fee of $2 to $5, or even for free if you choose not to tip. This narrative of ‘using what you own’ rather than ‘borrowing what you don’t have’ is a powerful shift in personal finance management.

[IMAGE_PROMPT: A high-quality close-up of a smartphone screen showing a modern banking app interface with a ‘Cash Advance’ button, surrounded by blurry city lights at night.]

Personal Loans from Online Lenders

For those with fair to good credit, a small personal loan from an online lender can be a game-changer. While traditional banks might not bother with loans under $1,000, many online fintech companies specialize in micro-loans. These loans typically carry APRs ranging from 6% to 36%, which is a fraction of the cost of a payday loan.

What makes these loans particularly attractive is the fixed repayment schedule. You receive the funds in a lump sum and pay them back in equal monthly installments over a year or more. This predictability allows for better long-term budgeting. It is important, however, to shop around and compare ‘pre-qualification’ offers to find the lowest rate without affecting your credit score.

Peer-to-Peer (P2P) Lending

If you prefer a more community-driven approach, Peer-to-Peer lending platforms like Prosper or LendingClub connect individual borrowers with individual investors. Because these platforms cut out the middleman (the bank), they can often offer lower rates. Investors are looking for a better return than a savings account, and borrowers are looking for a lower rate than a credit card or payday loan. It’s a win-win scenario that relies on a narrative of mutual benefit rather than institutional profit.

The 0% Interest Credit Card Strategy

While it may seem counterintuitive to fight debt with a credit card, cards with a 0% introductory APR on purchases can be a powerful tool—if used with extreme discipline. If you have a decent credit score, you might qualify for a card that charges no interest for the first 12 to 18 months. This allows you to pay off an emergency expense over several months without a single penny going toward interest. However, the caveat is clear: if the balance isn’t paid off before the introductory period ends, the interest rate will jump significantly.

Local Non-Profits and Community Resources

Sometimes, the best alternative isn’t a loan at all. Many community organizations, religious institutions, and non-profits offer emergency financial assistance for things like utility bills, rent, or medical expenses. Organizations like the St. Vincent de Paul Society or local Community Action Agencies provide grants or low-interest ‘rescue’ loans to help families stay afloat. These programs are rooted in the philosophy of community support, aiming to lift individuals out of poverty rather than profiting from their struggle.

Building a Financial Buffer for the Future

While finding an alternative to a payday loan solves the immediate crisis, the ultimate goal should be to break the cycle permanently. This involves two main strategies: credit building and emergency savings.

Even a small ‘starter’ emergency fund of $500 can prevent 90% of the situations that lead people to payday lenders. Simultaneously, using tools like ‘credit builder loans’ can help improve your credit score, ensuring that the next time you need to borrow, you qualify for the lowest possible interest rates.

Conclusion

The story of high-interest payday loans is often one of desperation, but it doesn’t have to be your story. By exploring credit union PALs, utilizing modern cash advance apps, or seeking community assistance, you can manage life’s unexpected hurdles without compromising your financial future. Remember, the best loan is the one that gives you the flexibility to breathe, not the one that takes your breath away. Choose alternatives that respect your hard work and provide a clear path back to financial stability.